Many investors discover terms like pledge, margin, and lien only after receiving an unexpected notification from their broker or depository participant. The confusion is understandable. These terms sound similar, yet they have very different implications for your investments.

For some investors, the concern goes deeper. A message indicating that shares have been pledged or marked under a lien can create anxiety about whether their investments remain safe and accessible. Without clarity, it becomes difficult to understand what rights you still hold over those securities.

The good news is that pledge, margin, and lien are well-defined mechanisms within India’s securities ecosystem. Understanding how they work can help you avoid surprises and make better decisions when using your investments as collateral.

This guide explains demat account pledge margin lien concepts in simple language, helping investors understand the difference between them and when each may apply.

On this page

Key Definitions: Pledge, Margin Pledge & Lien

Before understanding the differences, here’s what each term means:

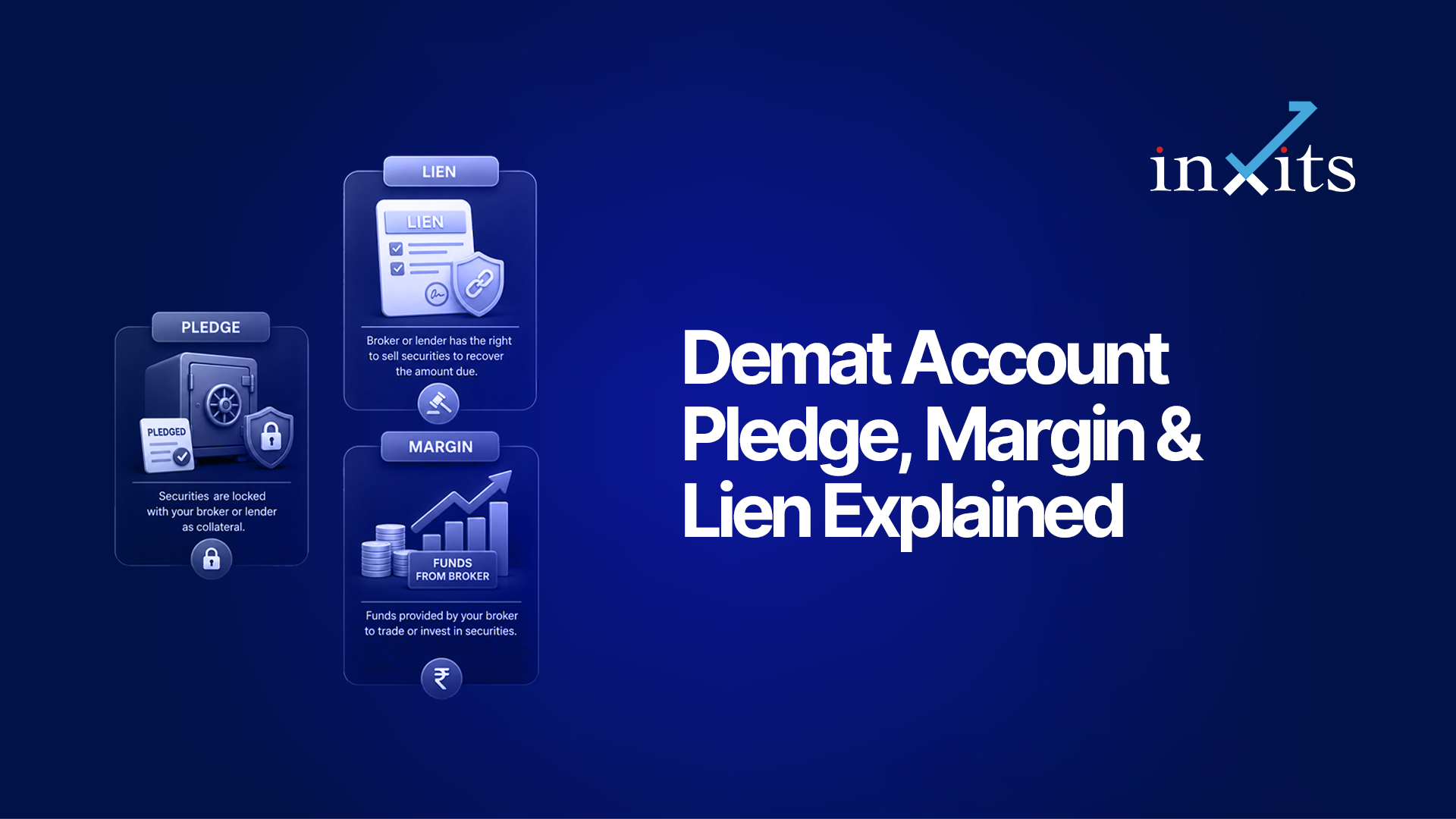

Pledge: Using securities as collateral while retaining ownership. The investor authorises the pledge, and the securities remain in their demat account.

Margin Pledge: A SEBI-introduced mechanism where securities are pledged specifically to meet trading margin requirements. The investor’s explicit approval is required before the pledge becomes active.

Lien: A legal claim over securities by a bank or financial institution until a financial obligation is fulfilled. Ownership remains with the investor, but the securities cannot be freely used or transferred while the lien exists.

Demat Account Pledge Margin Lien in India: Key Takeaways

Before getting into the details, keep these points in mind:

- A pledge allows securities to be used as collateral while ownership remains with the investor.

- Margin pledges are commonly used for trading and derivative positions.

- A lien creates a legal claim over securities under specific circumstances.

- Securities under pledge generally remain in your demat account.

- SEBI regulations have increased transparency around margin pledging.

What Is a Pledge in a Demat Account?

A pledge allows an investor to use securities as collateral for borrowing money or obtaining trading limits without transferring ownership.

When shares are pledged, they continue to remain in the investor’s demat account. However, a lender or broker receives certain rights over those securities if the investor fails to meet agreed obligations.

An investor holding shares worth ₹5 lakh may pledge them to get trading margin or a loan. The shares stay in their demat account and show a “pledge” marking, but they cannot be freely sold until the pledge is released.

The key point is simple: ownership stays with the investor, while the pledged securities serve as security for an obligation.

How Does Share Pledging Work?

The process generally follows these steps:

- The investor submits a pledge request.

- The broker or lender initiates the pledge through the depository system.

- The investor authorises the request.

- The securities receive a pledge marking.

- Collateral value is assigned based on approved haircuts.

Because the process is electronic, investors can verify pledge status directly through their depository records.

Can Pledged Shares Still Earn Benefits?

Yes. In most cases, investors continue receiving corporate benefits such as:

- Dividends

- Bonus shares

- Rights entitlements

- Stock splits

However, specific terms may vary depending on the arrangement and the institution involved.

What Is Margin Pledge and Why Was It Introduced?

Margin pledge is a mechanism introduced to improve investor protection and transparency.

Before the regulatory changes introduced by the Securities and Exchange Board of India (SEBI), brokers often transferred client securities into pooled accounts for margin purposes. This created concerns about misuse and reduced visibility for investors.

Under the current framework, securities remain in the investor’s demat account while being pledged for margin requirements.

Why Is Margin Pledge Different from Traditional Pledge?

A margin pledge is specifically designed to support trading activities.

The collateral value of pledged securities can be used for:

- Equity trading

- Futures and options positions

- Margin requirements

- Risk management obligations

Because the securities stay within the investor’s account, transparency improves significantly.

Many investors mistakenly assume that a margin pledge means the broker owns the shares. That is not correct. The investor continues to hold ownership while allowing the securities to support approved trading activities.

Key Facts on Margin Pledge

- Introduced under SEBI’s margin pledge framework.

- Securities remain in the investor’s demat account.

- Collateral value depends on approved haircuts.

- Investors receive pledge confirmation directly from the depository.

- Unauthorised pledges require investor approval before activation.

What Is a Lien on Securities?

A lien is a legal right that allows an institution to retain a claim over securities until a specific obligation is fulfilled.

Although pledge and lien are related concepts, they are not identical.

A lien may arise when securities are used to secure obligations with banks, financial institutions, or other authorised entities.

The holder of the lien gains a legal claim over the securities. However, ownership does not automatically transfer.

When Can a Lien Be Created?

Common situations include:

- Loan against securities arrangements

- Borrowing against investment portfolios

- Certain banking relationships

- Regulatory or legal obligations

For investors considering a loan against mutual funds, understanding lien mechanics becomes particularly important because financial institutions may use similar collateral structures.

Pledge vs Lien: What Is the Difference?

| Feature | Pledge | Lien |

| Purpose | Collateral for borrowing or margin | Legal claim over securities |

| Ownership | Remains with investor | Remains with investor |

| Activation | Through pledge process | Through contractual or legal arrangement |

| Common Use | Trading margin (equity, F&O) and loans against securities | Bank loans against securities, regulatory or legal obligations |

| Enforcement Rights Depository Visibility | Defined by pledge agreement Visible as pledge marking in CDSL/NSDL account | Defined by lien terms Visible as lien marking in CDSL/NSDL account |

Investors often use the terms interchangeably. However, the underlying legal structures can differ.

What Risks Should Investors Understand?

Pledging securities is a recognised and regulated process. Nevertheless, investors should understand the associated risks before proceeding.

Invest Smarter.

Grow Confidently.

Your AI-powered SEBI-registered investment advisor — with research you can trust and insights that grow with you.

Download inXits Free

What Happens If Obligations Are Not Met?

If an investor fails to meet repayment or margin requirements, the lender or broker may invoke the pledge.

Once invoked, the securities can be sold or transferred according to applicable rules and contractual terms.

Therefore, investors should monitor:

- Margin utilisation

- Loan repayment schedules

- Collateral value changes

- Market volatility

Does Market Volatility Affect Pledged Securities?

Yes. Falling market prices can reduce collateral value.

A portfolio worth ₹10 lakh pledged as margin may have a collateral value of ₹8 lakh after a standard haircut. If markets fall 20%, the portfolio drops to ₹8 lakh, but collateral value falls to ₹6.4 lakh, potentially triggering a margin call.

Many experienced investors view pledged securities as a financing tool rather than a source of extra leverage. That mindset often helps maintain better risk control.

Not sure whether borrowing against investments is affecting your overall financial plan? A review with a financial advisor can help assess whether your current portfolio structure aligns with your long-term goals.

How Can Investors Use Pledge Facilities Responsibly?

The most effective use of pledging begins with understanding the purpose behind it.

Investors generally use pledges for one of three reasons:

- Accessing liquidity without selling investments.

- Meeting trading margin requirements.

- Supporting short-term financing needs.

Before pledging securities, consider:

- The borrowing cost involved.

- The quality of the pledged assets.

- Potential margin calls during volatile periods.

- Alternative sources of liquidity.

For investors focused on long-term portfolio management, asset allocation and risk management often matter more than temporary borrowing flexibility. A structured approach generally reduces the chances of forced decisions during market stress.

Also check: Portfolio rebalancing

How inXits Helps Investors Evaluate Portfolio Risks

Understanding demat account pledge margin lien arrangements is only one part of managing investments effectively. The larger question is whether borrowing decisions fit within your overall financial strategy.

At inXits, advisors help investors evaluate portfolio structure, risk exposure, liquidity needs, and long-term objectives. Rather than focusing only on available collateral value, the discussion centres on how financial decisions affect future goals.

Many investors wonder whether they should pledge securities, sell investments, use alternative funding sources, or adjust portfolio allocations. The answer depends on individual circumstances rather than a one-size-fits-all approach.

If you want clarity on how borrowing, margin usage, or collateral decisions fit into your broader financial plan, speaking with a SEBI registered financial advisor can help you assess available options objectively.

Conclusion

The terms pledge, margin pledge, and lien often create confusion because they all involve securities being used as collateral in some form. However, each serves a different purpose within India’s financial system.

A pledge allows securities to support borrowing while ownership remains with the investor. A margin pledge specifically supports trading-related collateral requirements under SEBI’s framework. Meanwhile, a lien creates a legal claim over securities until certain obligations are fulfilled.

Understanding demat account pledge margin lien concepts can help investors avoid misunderstandings, monitor risks more effectively, and make informed decisions about using investments as collateral. As financial products become more sophisticated, knowing how these mechanisms work becomes an important part of responsible portfolio management.

If you are unsure whether your current borrowing or collateral strategy aligns with your financial goals, consulting an investment advisor can provide a clearer perspective on potential risks and opportunities.

Frequently Asked Questions

What is a pledge in a demat account?

A pledge in a demat account allows investors to use securities as collateral for borrowing or margin purposes. Ownership generally remains with the investor while the securities support an obligation.

What is the difference between pledge and margin pledge?

A traditional pledge can support borrowing arrangements, while a margin pledge is designed specifically for trading collateral requirements. Under the margin pledge framework, securities remain visible in the investor’s demat account.

What is a lien on securities?

A lien is a legal claim over securities that remains in place until a financial obligation is satisfied. Ownership does not automatically transfer, but the institution holding the lien gains specific rights.

Can I sell pledged shares?

In many situations, pledged shares cannot be freely sold unless the pledge is released or adjusted. The exact process depends on the lender, broker, and agreement terms.

Do I receive dividends on pledged shares?

Generally, investors continue receiving dividends and other corporate actions while shares remain pledged. However, specific arrangements should always be reviewed carefully.

Is margin pledge regulated by SEBI?

Yes. The Securities and Exchange Board of India regulates the margin pledge framework to improve transparency, investor protection, and collateral management practices.

Can banks place a lien on demat securities?

Yes. Banks and authorised financial institutions may create a lien when securities are used as collateral for approved lending arrangements.

What happens if a pledge is invoked?

If obligations are not fulfilled, the lender or authorised party may invoke the pledge according to the agreement. The securities may then be sold or transferred to recover outstanding dues.

Is pledging securities better than selling investments?

The answer depends on individual circumstances. Pledging may provide liquidity while retaining investment exposure, but it also introduces borrowing obligations and collateral-related risks.

Disclaimer

Investments in securities markets are subject to market risks. Read all related documents carefully before investing.

inXits is a SEBI-registered investment adviser (Registration No. INA000020369). This article is for educational purposes only and does not constitute personalised investment advice.

Registration granted by SEBI, membership of BSE, and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

Himani Barot, CFP, is a Principal Officer at inXits with 4+ years of experience in portfolio management, investment advisory, and comprehensive financial planning. As a Certified Financial Planner, she helps clients navigate complex financial goals with structured, personalised strategies.