Many investors build portfolios by investing in multiple mutual funds across categories. At first glance, this approach appears diversified because it spreads investments across different schemes. However, the underlying holdings of those funds may sometimes include the same stocks or securities.

This situation is known as mutual fund overlap, and it is more common than many investors realize. When investors select funds based only on category names or past popularity, they may unknowingly hold multiple funds that invest in similar companies.

As a result, the portfolio may appear diversified on the surface but still carry concentration in certain stocks or sectors. Therefore, understanding mutual fund overlap helps investors better interpret how diversification works in mutual fund portfolios.

This article explains what mutual fund overlap means, why it occurs, how investors evaluate it, and how it fits into a broader framework of portfolio analysis.

What Is Mutual Fund Overlap?

Mutual fund overlap refers to a situation where two or more mutual funds in an investor’s portfolio hold the same underlying securities.

For example, two different equity mutual funds may both hold shares of the same large companies.

A simplified illustration:

| Mutual Fund | Major Holdings |

| Fund A | Company A, Company B, Company C |

| Fund B | Company A, Company D, Company E |

In this example, Company A appears in both funds, which creates overlap.

The securities quoted are for illustration only and are not recommendatory.

While some level of overlap may occur naturally, a high degree of overlap may reduce the intended diversification of the portfolio.

Understanding mutual fund overlap allows investors to look beyond the scheme name and focus on the actual composition of investments.

Why Mutual Fund Overlap Happens

Several factors contribute to the occurrence of mutual fund overlap in investor portfolios.

Similar Investment Strategies

Many funds follow similar investment philosophies. For instance:

- Large-cap equity funds often invest in the same set of established companies

- Index funds replicate benchmark indices

- Sector funds focus on specific industries

Because of these strategies, different funds may hold overlapping securities.

Benchmark-Based Investing

Mutual funds often track or benchmark themselves against market indices such as Nifty or Sensex.

When multiple funds follow the same benchmark, their portfolios may include similar companies.

Popular Large-Cap Companies

Large and well-known companies often appear across multiple portfolios because of their market capitalization and liquidity.

Example illustration:

| Company | Presence in Multiple Funds |

| Company X | Fund A, Fund B, Fund C |

| Company Y | Fund B, Fund D |

The securities quoted are for illustration only and are not recommendatory.

Therefore, the presence of common holdings across funds contributes to mutual fund overlap.

Investors Holding Multiple Funds in the Same Category

Another reason for overlap is when investors allocate money to several funds within the same category.

Examples may include:

- Two large-cap funds

- Multiple flexi-cap funds

- Several index funds tracking similar benchmarks

In such cases, overlapping portfolios can naturally occur.

How Mutual Fund Overlap Affects Portfolio Diversification

Diversification aims to spread investments across different assets to reduce concentration risk.

However, mutual fund overlap may affect diversification in the following ways.

Reduced True Diversification

Although an investor may hold several funds, overlapping holdings may lead to concentration in certain companies.

For example:

| Portfolio | Actual Exposure |

| 4 Funds | Large allocation to same 5 companies |

The securities quoted are for illustration only and are not recommendatory.

This means the effective diversification may be lower than expected.

Similar Portfolio Movements

If multiple funds hold the same companies, their performance may move in similar directions when those stocks change in value.

As a result, the portfolio may respond similarly to market changes.

Duplication of Investment Strategy

When two funds follow similar strategies and hold similar securities, the investor may effectively hold duplicate exposure.

This does not necessarily mean the funds are unsuitable. However, it highlights the importance of understanding the underlying portfolio composition.

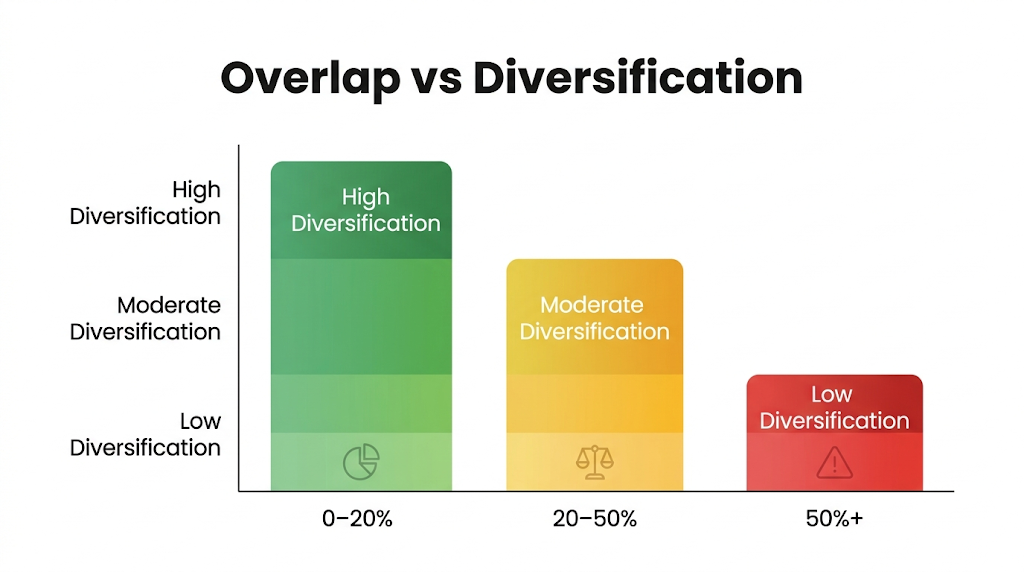

Overlap vs Diversification

This chart shows how increasing mutual fund overlap can reduce overall portfolio diversification.

Measuring Mutual Fund Overlap

Investors and analysts often measure mutual fund overlap by comparing the holdings of two funds.

This process generally involves examining:

- Top holdings

- Sector allocation

- Percentage weight of common securities

An example comparison may look like this:

| Company | Fund A Weight | Fund B Weight |

| Company A | 8% | 7% |

| Company B | 6% | 5% |

| Company C | 4% | 4% |

The securities quoted are for illustration only and are not recommendatory.

If a significant number of holdings match across two funds, the overlap level may be considered high.

Several analytical tools in the financial ecosystem allow investors to study portfolio holdings and identify overlaps.

Mutual Fund Overlap Percentage Formula

To quantify overlap between two mutual funds, investors often use an overlap percentage formula based on common holdings.

Overlap %=∑min(Weight in Fund A,Weight in Fund B)

This means comparing each common stock and taking the lower allocation between the two funds, then summing all such values.

Example (illustrative):

| Company | Fund A | Fund B | Min Weight |

| HDFC Bank | 8% | 7% | 7% |

| Reliance | 6% | 5% | 5% |

Total overlap = 7% + 5% = 12%

The securities quoted are for illustration only and are not recommendatory.

Tools to Check Overlap

Investors can use various platforms to analyze mutual fund overlap, such as:

- Fund house fact sheets (monthly portfolio disclosures)

- Financial research platforms

- Portfolio analysis tools offered by investment platforms

- Aggregators that compare fund holdings side by side

For example, investors can use the inXits Portfolio Overlap tool to compare mutual funds and identify overlapping holdings in a structured manner.

Real India Example:

Consider an example from the Indian market:

Two large-cap funds may both hold companies such as Reliance Industries, HDFC Bank, and ICICI Bank. Even though the funds are different, their top holdings may significantly overlap because they invest in a similar universe of large-cap stocks.

The securities quoted are for illustration only and are not recommendatory.

Ideal Overlap Level

There is no fixed ideal overlap, but general guidelines include:

- 0–20%: Low overlap (higher diversification)

- 20–50%: Moderate overlap

- Above 50%: High overlap (possible duplication of exposure)

The appropriate level depends on the investor’s strategy and portfolio structure.

When Overlap Is Dangerous

Overlap may become a concern in the following situations:

- Holding multiple funds in the same category

- High concentration in a few common stocks

- Similar investment styles across funds

- Market downturn affecting the same underlying holdings

In such cases, the portfolio may behave like a concentrated investment rather than a diversified one.

Situations Where Overlap May Naturally Occur

It is important to note that some degree of mutual fund overlap may occur naturally and does not always indicate a problem.

Large-Cap Fund Portfolios

Large-cap funds typically invest in a defined set of established companies.

Therefore, overlap across such funds may be expected.

Index Funds Tracking the Same Benchmark

Two index funds tracking the same index will naturally have nearly identical holdings.

Market Concentration

In markets where certain companies dominate index weight, multiple funds may include them as core holdings.

Therefore, understanding the structure of mutual funds helps investors interpret overlap appropriately.

Evaluating Portfolio Structure Beyond Overlap

While analyzing mutual fund overlap, investors often examine broader portfolio characteristics as well.

These may include:

Asset Allocation

Asset allocation refers to how investments are distributed across asset classes such as:

- Equity

- Debt

- Gold

- Cash equivalents

Sector Exposure

Some portfolios may show concentration in specific sectors.

Example illustration:

| Sector | Portfolio Exposure |

| Banking | 30% |

| Technology | 20% |

| Consumer Goods | 15% |

This structure may influence portfolio behavior during sector-specific market changes.

Investment Style

Funds may follow different styles such as:

- Growth investing

- Value investing

- Blend strategies

Understanding style differences helps interpret portfolio composition.

Example Scenario of Mutual Fund Overlap

Consider a hypothetical portfolio:

| Fund | Category |

| Fund A | Large Cap |

| Fund B | Flexi Cap |

| Fund C | Index Fund |

After examining holdings, an investor finds that the same five companies appear across all three funds.

The securities quoted are for illustration only and are not recommendatory.

In this scenario, the investor may observe that multiple funds share similar exposures.

This example demonstrates how mutual fund overlap can occur even when funds belong to different categories.

How Structured Portfolio Reviews Help Investors

Portfolio evaluation involves understanding how investments interact with each other rather than analyzing each fund individually.

Many investors review portfolios periodically to understand:

- Asset allocation balance

- Sector exposure

- Portfolio concentration

- Overlapping holdings

- Long-term financial goals

Approaching financial decisions through a structured framework—similar to how a personal CFO analyzes financial information—can help organize these factors more clearly.

Platforms such as inXits combine research frameworks and technology to help investors understand portfolio structures, diversification patterns, and financial planning considerations.

Connect with inXits for a 24×7 consultation focused on financial planning and portfolio review processes.

Conclusion

Mutual funds are widely used by investors to access diversified portfolios managed by professional fund managers. However, owning multiple funds does not automatically guarantee diversification.

Understanding mutual fund overlap helps investors examine the actual holdings within their portfolio and evaluate how different funds interact with each other.

Overlap can occur due to similar investment strategies, benchmark tracking, or concentration in large-cap companies. While some overlap may occur naturally, analyzing portfolio structure provides greater clarity about diversification and exposure.

Therefore, continuous learning, periodic portfolio reviews, and structured financial analysis play an important role in understanding how mutual fund investments fit within long-term financial planning.

Connect with inXits for a 24×7 consultation focused on financial planning and portfolio review processes.

📘 Disclaimer

Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

Registration granted by SEBI, membership of BSE and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

The securities quoted are for illustration only and are not recommendatory.